Assets

-

Brand & Reputation

Brand &

ReputationUnipolSai compared to the Insurance Sector:

‘Top of Mind’ December 2021*

Unipol compared to the Insurance Sector: reputation trends with the general public**

1 out of 4 Italians cites UnipolSai as the first insurance company that comes to mind (Top of Mind)

1 out of 4 Italians cites UnipolSai as the first insurance company that comes to mind (Top of Mind)- Unipol at maximum reputation levels in the insurance sector

- High credibility for innovative and evolving initiatives

* Source: First operator spontaneously mentioned - Research on the reputation and brand equity of insurance companies in Italy - Demoskopea Consulting - Research Custom Unipol 2021

** Source: The RepTrak Company™ - Research Custom Unipol 2019-2021 High brand equity and reputation as key factors to encourage customer loyalty

High brand equity and reputation as key factors to encourage customer loyalty

-

Customer base

15.5 mln

Group Customers 70% Clienti con interazione digitale

70% Clienti con interazione digitale 4 mln di download di app

4 mln di download di app 170 mln di minuti trascorsi su touch point digitali

170 mln di minuti trascorsi su touch point digitali 1 comunicazione diretta con i Clienti ogni 10 gg

1 comunicazione diretta con i Clienti ogni 10 gg 75% di Clienti contattabili

75% di Clienti contattabili

- The size of the Customer Base enhances the Insurance strategy and enables ecosystems approach

- Strong Customer engagement: most used app in the Italian insurance market, high levels of digital interaction and significant communication frequency

Broad Customer Base with high levels of engagement

-

Data & analytics

4,000

TeraByte of Data Over 4 mln telematic devices

Over 4 mln telematic devices 11 mln telematic services provided

11 mln telematic services provided  3.7 bn journeys recorded

3.7 bn journeys recorded Artificial Intelligence

Artificial Intelligence 800 mln interactions on Digital Touch Points

800 mln interactions on Digital Touch Points 25 mln logins on Digital Touch Points

25 mln logins on Digital Touch Points

Insurance Value Chain

Data and Analytics integrated along the insurance value chain and supporting the Beyond Insurance initiatives

Data and Analytics integrated along the insurance value chain and supporting the Beyond Insurance initiatives

-

Motor model

Over 10 mln

vehicles insured Distinctive Offer in terms of insurance and beyond insurance services

Distinctive Offer in terms of insurance and beyond insurance services Over 90 variables for motor pricing

Over 90 variables for motor pricing  Injuries management model

Injuries management model 800,000 post-accident interventions provided directly

800,000 post-accident interventions provided directly > 700,000 spare parts intermediated

> 700,000 spare parts intermediated 2,700 UnipolService body repair shops, 215 UnipolGlass centres

2,700 UnipolService body repair shops, 215 UnipolGlass centres

- Premium positioning in terms of offering a wide range of coverages and services

- Motor TPL market leader:

- - Current year Loss Ratio* (63.5% compared to 69.6%) - Current year settlement speed** (77.3% compared to 73.9%) - Current year average cost of paid claims** (€2,607 compared to €2,843)

- Full supervision of the claims management process to ensure financial efficiency and transparency

* UnipolSai compared to industry average (excluding UnipolSai); source: ANIA, 2020 figures

** UnipolSai compared to industry average (excluding UnipolSai); source: IVASS, 2020 figures

Distinctive, integrated Motor model as a key factor in Motor TPL market leadership

-

Health model

11 mln

Customers €750m premiums

€750m premiums Over 500 Operators Proprietary telephone operations centre

Over 500 Operators Proprietary telephone operations centre  51 healthcare funds managed

51 healthcare funds managed  60 doctors in the company

60 doctors in the company  4.3 mln claims managed

4.3 mln claims managed  Over 20,000 affiliated medical centres in Italy and abroad

Over 20,000 affiliated medical centres in Italy and abroad

- Leading Group in the Italian Health business

- Single integrated model of insurance management and service development

- Network with the best public and private affiliated healthcare facilities

- Direct provision of services offered by UniSalute

Integrated Health Model as a key element for further development of the Group’s leadership

-

Agency Network

> 2,100

Agencies Agreement 2.0 Partnership with the Network

Agreement 2.0 Partnership with the Network  30,000 professionals

30,000 professionals  750,000 leads from digital channels

750,000 leads from digital channels  ~ 600 agents under 45

~ 600 agents under 45 2,000 Insurance and Beyond Insurance specialists

2,000 Insurance and Beyond Insurance specialists  8,000 sales points on average reachable within 10 minutes from home

8,000 sales points on average reachable within 10 minutes from home

- Consolidated partnership based on shared strategy, targets and economics

- Specialisation of the Agency Network overseeing the different market segments

- High-Performing distribution network including for the Beyond Insurance initiatives

Central role of the Agency Network in the evolution of the Group’s strategies

-

Banking Networks

Banking

Networks- 2,612 Number of branches

- ~5.9 mln Customers

- ~10% Non-Life Insurance penetration * span>

- Unique bancassurance model (Arca Vita and Arca Assicurazioni are dedicated companies with about 400 employees) that enhances Unipol Group assets in favour of the bancking partners

- Strong oversight of the banking channel in terms of both local presence and target customers

* Estimate based on BPER and BP Sondrio customer base

Banking networks with high growth potential in terms of insurance penetration of their customer base

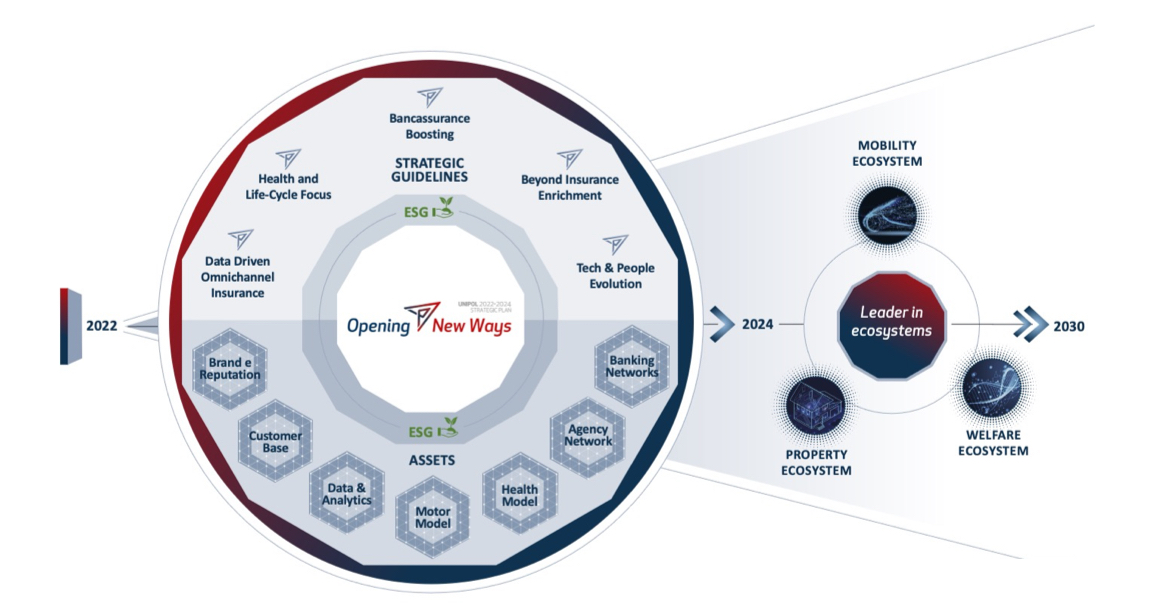

Strategic guidelines

Consolidate the Group's technical and distribution excellence, through an increasingly intensive use of Data and Analytics:

- Pricing and Underwriting - Develop algorithms based on internal and external data, to improve retention, conversion and profitability models

- Settlement - Develop claims settlement model to manage injuries, performance of the settlement networks and full use of the direct and affiliated network for the direct repair

- Launch of a Digital Venture, BeRebel

- Phygital sales process – Massive generation of new opportunities through digital channels

- Targeting - Improve sophistication of commercial proposals based on data-driven algorithms

Develop a new platform for the Retail insurance offer, by exploiting the effectiveness of the leading agency network and completing the omnichannel evolution of the distribution model:

- Evolution of the retail offer which is distinctive in terms of volume and depth

- Greater richness and usability of information, to accelerate technical excellence

- Personalise the offer through needs assessments

- Full omnichannel distribution strategy with a central role of the agency network boosted by the contribution from the digital channels

- Develop a distinctive customer experience on all touch points

- Reduce time-to-market of products and services

- 24/7 availability of transactions for customers and agents

Strengthen leadership in the health business by enhancing the UniSalute centre of excellence in support of all the Group's Distribution Networks:

- Use the brand, skills and know-how of UniSalute on all the group distribution networks

- Introduce a targeting and needs assessment model based on the customer's needs at the different life-cycle stages

- Develop a supplementary health offering for the members of the funds

- Strengthen the chronic disease management programmes

- Develop digital health services including telemedicine

- Develop TPA services mainly in the welfare area

Life products offer with a Life-Cycle perspective and optimised capital absorption:

- In the savings area, focus on annual premiums and supplementary pensions

- Enhance the offer and distribution capacity in the protection business

- Focus on capital light products in the investment area

Strenghten the bancassurance business model by enhancing the Group’s distinctive capabilities for the benefit of the banking partners:

- Develop the non-life and life protection segment both on a stand-alone basis or bundled with banking products

- Maximise commercial effectiveness by creating a joint “data and event driven” targeting model

- Introduction of insurance specialists

- New incentive schemes

- Synergies among distribution networks for broader coverage of SME customer needs

- New digital tools and sales processes

Accelerate the evolution of the Group’s offer by futher extending the Mobility ecosystem and strengthening the Welfare and Property ecosystems:

- Unipol will become a 360° partner in the Mobility area, consolidating its position along the entire life cycle of Mobility Life Cycle, especially through UnipolRental and UnipolMove

- Within the scope of the Welfare ecosystem, Unipol will develop further initiatives to strengthen its own position, especially through proprietary medical centres development, digital health services including telemedicine and launch of a new flexible benefits platform

- Within the Property ecosystem, Unipol shall become a reference player in home and apartment building related services, creating standalone value and contributing to Group synergies, especially developing a network of tradespeople and managing a network of franchised administrators

Digital evolution in the operating model through intensive use of new technologies, data, automation and the evolution of the company’s organisation:

- Digitalise core systems and pursue process automation

- Develop digital platforms

- Improve application architectures and technological infrastructures

- Cybersecurity

- Artificial intelligence to further improve the operating model and reduce activities with low added value

- Generational change also through the solidarity fund which strengthens specialisation and new skills

- Extensively increase accountability on industrial plan targets

- Digital workplace

Target and KPI

-

Insurance KPIs

Insurance KPIs

2024 Target Δ vs 2021 Non-Life Premiums €8.9bn + 4.5% CAGR of which Motor €4.2bn + 3.1% CAGR of which non-Motor* €3.7bn + 4.7% CAGR of which Health €1.0bn + 10.0% CAGR CoR Non-Life (net of reinsurance) 92.6 % - 2.7 p.p. Life premiums €5.8bn + 2.5% CAGR Present Value Future Profit Margin 3.5 % + 0.5 p.p. * Excludes Health Business

-

Financial and Sustainability KPIs

Unipol Group

2022-2024 TARGETUnipolSai

2022-2024 TARGETCumulative consolidated net profit* 2022-2024 €2,3bn €2,3bn Cumulative dividends 2022-2024 €0.75bn €1.4 bn 2024 Target Share of products with environmental and social value 30% Finance for the SDGs

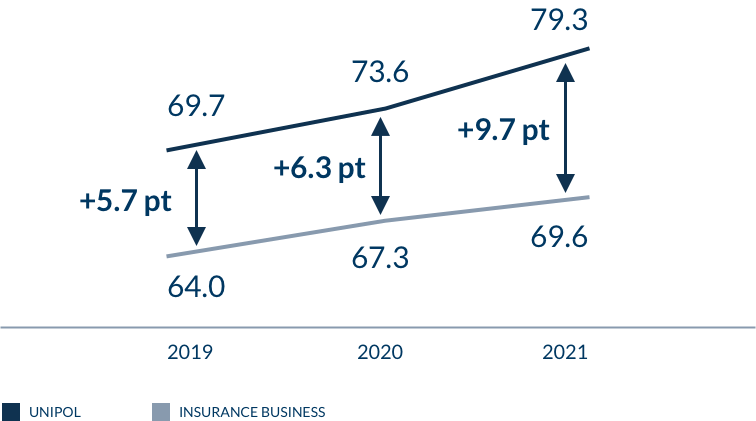

(increase in amount of thematic investments for the SDGs)€1.3bn Reputational Index

(reputation score among the general public

according to RepTrak® methodology)> Average insurance sector Unipol management incentive system 20% incentive long-term system linked to ESG targets * Consolidated normalised profit (excluding Employee Solidarity Fund) calculated on the basis of current accounting standards